Maker vs Taker Fees Explained: How Order Type Silently Sets Your Real Crypto Exchange Cost

Two traders can place the exact same order — same exchange, same coin, same dollar amount — and pay a completely different fee, simply because one order type adds liquidity to the market and the other removes it. That distinction is the maker/taker model, and it underpins the pricing on almost every centralized exchange. Most investors know the words “maker” and “taker” exist somewhere on a fee schedule; few realize how much control they actually have over which one they pay, or how far the gap widens at scale.

This article breaks down the mechanics using the actual published fee schedules of major exchanges, current 2026 VIP-tier data, and documented rebate structures — not a generic definition. It’s a companion piece to our Global Crypto Exchange Cost Map 2026, which ranks 12 platforms on fees, liquidity, security, withdrawal speed, and regulatory compliance, and builds on Crypto Trading Fees Explained: How Exchange Costs Affect Long-Term Investment Returns, which shows how small, recurring fee differences compound into large gaps over a multi-year holding period.

What “maker” and “taker” actually mean

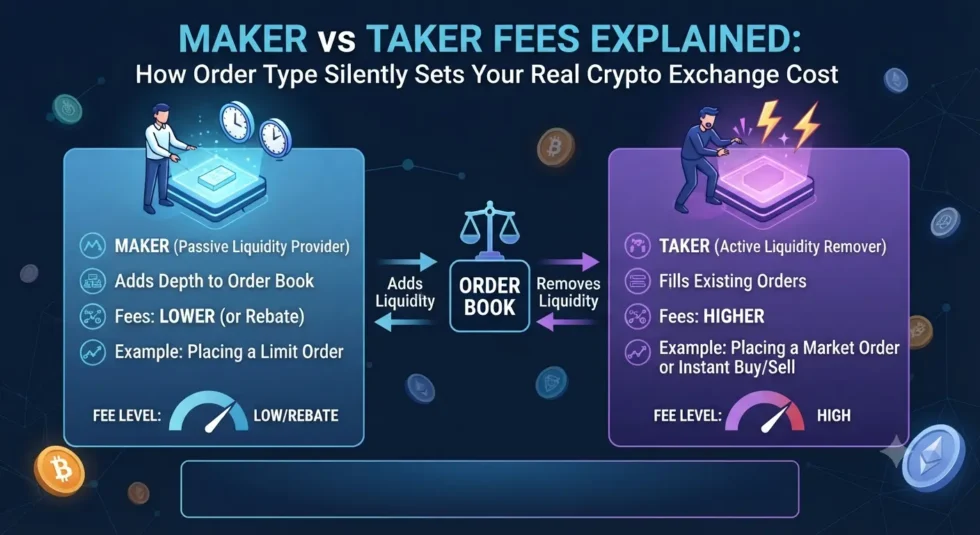

Every trade on an order-book exchange has two sides: the order that was already sitting on the book, and the order that just arrived and matched against it.

- A maker order adds liquidity. It’s a limit order placed at a price that isn’t immediately matched, so it rests on the order book waiting for someone else to trade against it. Because it deepens the book and gives other traders something to trade into, exchanges reward it with a lower fee.

- A taker order removes liquidity. It’s a market order, or a limit order priced aggressively enough to match instantly against an existing order on the book. Because it consumes liquidity that was already there, exchanges charge it a higher fee.

The mechanism is simple, but the financial impact is not small. Exchanges structure pricing this way because order-book depth is what makes an exchange usable in the first place — thin books mean wide spreads and unreliable execution, so makers are effectively being paid to do the work of keeping the market functional.

The base-tier gap, exchange by exchange

At the entry level — no volume discounts, no native-token holdings — the maker/taker spread varies enormously by platform. Based on official 2026 fee schedules:

- Binance: 0.10% maker / 0.10% taker on spot (identical at base tier), dropping to 0.075%/0.075% with the BNB payment discount. Futures start at 0.02% maker / 0.05% taker.

- Kraken: 0.25% maker / 0.40% taker on Kraken Pro at the lowest tier (some sources cite 0.16%/0.26% depending on the exact schedule version), with futures starting at 0.02%/0.05%, matching Binance and OKX.

- Coinbase Advanced Trade: 0.40%–0.60% maker / 0.60%–1.20% taker at the lowest volume tier — among the widest base-tier spreads of any major exchange.

- OKX: 0.08% maker / 0.10% taker on spot at the retail tier.

- Bybit: 0.10% maker / 0.10% taker on spot; 0.02% maker / 0.055% taker on perpetual futures.

- MEXC: 0% maker / 0.05% taker on spot — the most aggressive maker incentive among major exchanges — and 0% or 0.01% maker / 0.04% taker on futures.

The spread between maker and taker fees is itself informative. On MEXC’s futures market, taker fees run roughly 4x the maker rate. On Coinbase Advanced’s base tier, the taker fee can run 2–3x the maker fee. A trader who defaults to market orders on Coinbase Advanced, without ever checking the order type, is paying up to three times what a limit-order trader pays for functionally the same trade.

Why the gap gets wider, not narrower, at scale

Volume-based VIP tiers don’t just lower fees uniformly — they tend to widen the relative gap between maker and taker rates, because exchanges want their largest traders providing the deepest liquidity.

Binance’s VIP ladder illustrates this clearly. At the base tier, spot maker and taker fees are identical at 0.10%. By VIP 5 (roughly $150 million in trailing 30-day volume), rates diverge to approximately 0.025% maker / 0.031% taker. At VIP 9, the top published tier, spot fees fall to roughly 0.00825% maker / 0.01725% taker — a maker rate that’s less than half the taker rate at that tier, compared to being identical at the bottom.

Futures markets push this further into negative territory. Kraken’s futures schedule matches the industry-standard 0.02% maker / 0.05% taker at the base tier, but at its highest published tier — $1 billion or more in monthly futures volume — the maker fee turns negative, at approximately −0.006%, while the taker fee settles around 0.0135%. At that tier, Kraken is literally paying traders a rebate to post limit orders, because deep, tight order books at that scale are worth more to the exchange than the fee itself. Similar negative-maker-fee rebate structures exist on Bybit’s and BitMEX’s top institutional tiers, though these are generally invitation-only or require sustained qualifying volume and minimum quoting requirements across multiple pairs.

The practical implication: the maker/taker distinction matters more, not less, as trading activity scales up. A retail trader ignoring order type at the base tier is leaving a fraction of a percent on the table. A high-volume trader ignoring it at the top tier is potentially forfeiting a rebate and paying a fee simultaneously — a full percentage-point swing in the wrong direction.

The catch: “maker” only applies if your order doesn’t fill immediately

The most common mistake isn’t misunderstanding the fee structure — it’s assuming that placing a limit order automatically qualifies for the maker rate. It doesn’t. A limit order only earns the maker fee if it rests on the book without immediately matching an existing order. If you place a limit buy order at or above the current best ask price, it executes instantly against existing liquidity and is charged as a taker order, regardless of the fact that you used the “limit order” button.

This distinction trips up investors who believe they’re consistently getting maker rates simply because they never click “market order.” In fast-moving markets, a limit order placed even slightly too aggressively — trying to guarantee a fill — crosses the spread and pays the taker rate. The only way to reliably capture the maker rate is to place a limit order at a price that has not yet been reached, and be willing to wait for the market to come to you.

Where the maker/taker model doesn’t apply — and why that’s a hidden cost of its own

Not every exchange interface uses maker/taker pricing, and the alternative is usually worse for the end user, not better. Coinbase’s standard “Simple” buy/sell screen, Kraken’s “Instant Buy,” and Binance’s “Convert” feature all price trades through a spread embedded in the quoted rate rather than a disclosed maker/taker fee. Because there’s no order book interaction on these interfaces — every trade is effectively a taker-equivalent transaction priced at whatever spread the exchange sets — investors on these screens never have the option to earn a maker rate at all. This is covered in more detail in our companion piece on hidden crypto exchange fees, which breaks down how much these spread-based interfaces cost relative to the advanced trading view on the same exchange.

The upshot is the same lesson from a different angle: the maker/taker model is not a tax you’re stuck paying — it’s a discount you’re eligible for only on interfaces that expose an order book. Using an exchange’s default “buy” button forfeits access to it entirely.

How to actually capture the maker rate

Three things determine whether a given order earns maker or taker pricing, and all three are within a trader’s control:

- Use the exchange’s advanced/pro trading interface, not the simplified buy/sell screen. Order-book access is a prerequisite for maker pricing to exist at all.

- Place limit orders below the current ask (for buys) or above the current bid (for sells), so the order rests on the book instead of matching instantly.

- Track 30-day trailing volume against the exchange’s VIP schedule. Because tiers recalculate on a rolling basis, consolidating trading activity onto a single exchange — rather than splitting it across several — can be the difference between a base-tier rate and a meaningfully discounted one, without changing total trading volume at all.

For traders evaluating exchanges specifically on execution cost, the full comparison across trading fees, liquidity depth, security track record, withdrawal speed, and regulatory standing is in the Global Crypto Exchange Cost Map 2026. And for the compounding math on how a maker-vs-taker habit affects returns over a multi-year holding period, see Crypto Trading Fees Explained: How Exchange Costs Affect Long-Term Investment Returns.